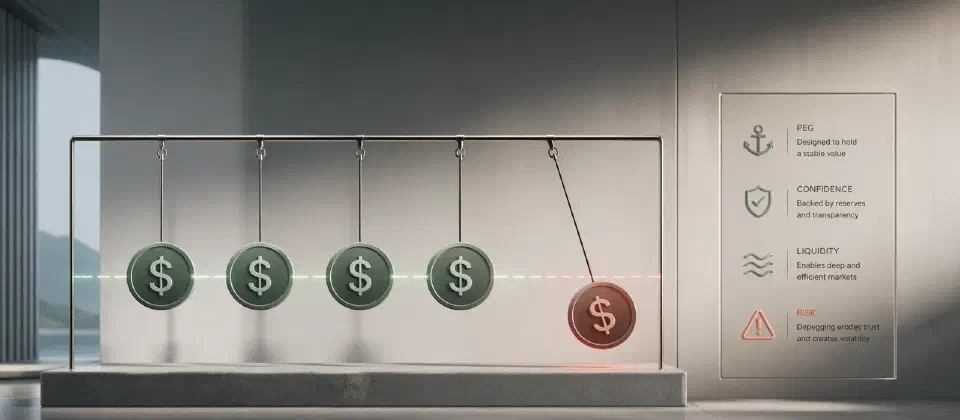

A stablecoin depeg is when a stablecoin loses its expected 1-to-1 anchor to the asset it tracks — most commonly the U.S. dollar. Instead of trading at $1.00, it might trade at $0.95, $0.80, or in extreme cases far lower. Sometimes a depeg is brief and self-correcting. Sometimes it is the beginning of a complete collapse.

The word “depeg” sounds technical, but the concept is straightforward: a stablecoin promised stability, and that promise is under stress or has broken. Understanding why that happens, how different stablecoin designs respond to that stress, and what the consequences look like for the broader market is one of the more useful pieces of crypto literacy a reader can develop — especially because the risk is not limited to people who hold the stablecoin in question.

How stablecoins are supposed to hold their value

Every stablecoin is built around a mechanism for maintaining its peg. The mechanism varies significantly by design, but they all come down to one of three foundations: real assets, collateral, or algorithmic incentives.

Fiat-backed stablecoins like USDC and USDT hold the peg through reserves. The issuer holds cash, short-term government securities, or similar assets roughly equivalent in value to the number of tokens in circulation. If someone wants to redeem one USDC for one dollar, the issuer can provide it. The peg holds as long as the reserves are real, accessible, and large enough to satisfy redemption demand.

Crypto-collateralized stablecoins like DAI hold the peg through over-collateralization. A user locks up more in cryptocurrency than the stablecoin value they receive — for example, depositing $150 worth of ETH to mint $100 worth of DAI. The extra buffer is there to absorb price swings in the collateral before the peg is threatened. If the collateral falls far enough, the position gets liquidated automatically to preserve backing.

Algorithmic and design-driven stablecoins attempt to hold the peg through supply and incentive mechanisms rather than direct backing. When the token trades above $1, the protocol expands supply to bring the price down. When it trades below $1, the protocol contracts supply or introduces incentives to buy. These systems work during normal conditions but can fail violently when confidence breaks because they rely on participants believing in the mechanism in order for the mechanism to work.

For a broader grounding in how stablecoins function and why they matter across crypto, see What Are Stablecoins?.

What causes a depeg

A depeg can start from several directions. The root cause determines how dangerous it is and whether recovery is possible.

Redemption stress is the most direct form of pressure for fiat-backed stablecoins. If a large number of holders try to redeem at once — triggered by concern about the issuer, a regulatory action, or a market shock — the issuer must deploy reserves quickly enough to satisfy demand. If redemptions exceed what can be processed promptly, the stablecoin can trade at a discount on the open market even if the underlying reserves are intact. The discount reflects the friction of getting out, not the absence of backing.

Reserve doubts are related but distinct. If the market becomes uncertain about whether a reserve is as large, liquid, or high-quality as the issuer claims, holders may sell preemptively before they can redeem. Tether’s reserve composition has been a recurring source of this kind of uncertainty. Market participants who are not confident they can access full value on redemption will accept a discounted price in a liquid secondary market rather than wait for a redemption process they are not sure will deliver.

Collateral collapse is the primary risk for crypto-backed stablecoins. If the collateral asset falls faster than the liquidation mechanism can respond — in a rapid market crash, for example, or when the market for the collateral becomes illiquid — the backing behind the stablecoin can erode faster than the system is designed to handle. Over-collateralization provides a buffer, but it is a finite one.

Design flaws and reflexivity are the defining failure mode for algorithmic stablecoins. These systems can enter a self-reinforcing loop: the stablecoin falls below $1, the mechanism creates new incentive tokens to absorb the pressure, those tokens are sold, both tokens fall further, confidence collapses, and the mechanism fails entirely. The incentive structure that was supposed to defend the peg becomes the vehicle for its destruction once enough participants stop believing in it. This is not a hypothetical scenario — it describes the mechanism behind one of the most significant stablecoin failures in crypto history.

Contagion and liquidity shocks can depeg stablecoins that are otherwise well-backed. When a major stablecoin fails, panic can spread to stablecoins that are structurally sound. If every large holder of stablecoins moves to reduce exposure simultaneously, even a well-reserved stablecoin can briefly trade below peg simply because sellers outnumber buyers in the immediate market. This kind of depeg is usually shallow and temporary, but it is still real.

The difference between a small drift and a serious event

Not every deviation from $1.00 is a crisis. Stablecoins trade on public markets, and small price dislocations are normal microstructure — buy and sell pressure does not always balance perfectly in real time. A stablecoin trading at $0.998 or $1.003 is within normal tolerance. It does not indicate a systemic problem.

The distinction that matters is whether the mechanism itself is functioning. A stablecoin at $0.98 during a period of unusually high redemption volume, where the issuer is processing withdrawals and the discount is likely to close once pressure eases, is a different situation from a stablecoin at $0.98 where the mechanism designed to restore the peg is clearly under stress and the market has lost confidence in the issuer or the design.

The signal that separates a manageable deviation from a serious depeg is reflexivity. When a stablecoin falls below peg and market participants respond by selling more — rather than buying the discount or redeeming — it means the market no longer believes the mechanism will restore $1.00. At that point, the depeg is self-reinforcing, and without intervention or a credible resolution to the confidence problem, the spiral tends to continue.

Recovery from a serious depeg requires restoring confidence in the mechanism itself: demonstrating reserves are intact, improving transparency, executing a bailout from an external party, or restructuring the protocol. None of those are quick or certain. When confidence is gone, the token has already effectively stopped functioning as a stablecoin regardless of the theory behind it.

Why depegs matter beyond the direct holder

The consequences of a stablecoin depeg rarely stay contained to the people holding that specific token. Stablecoins are embedded deeply enough in crypto infrastructure that a serious depeg ripples outward.

DeFi protocols use stablecoins as collateral. When a stablecoin depegs, any protocol that accepted it at face value is now holding an asset worth less than it priced. That creates a cascade of undercollateralized positions, forced liquidations, and protocol solvency questions. The stress spreads through the lending and liquidity layers of the ecosystem whether or not those protocols were the original source of the problem.

Major stablecoins also serve as the settlement layer for crypto exchange trading. If a widely used stablecoin depegs during a period of high market stress — which is exactly when liquidity is most needed — the settlement infrastructure for a large portion of crypto trades is impaired. Traders trying to move out of positions may find they cannot complete transactions at the prices they expect.

The contagion can reach assets far removed from the stablecoin itself. When confidence in stablecoins falls, traders move to reduce crypto exposure broadly, not just stablecoin exposure. A stablecoin crisis typically coincides with a sharp drop across crypto markets as holders liquidate positions to access fiat rather than remain in any part of the ecosystem.

Understanding how crypto prices reflect market structure — not just supply and demand for individual tokens — is a useful companion to this topic. See Crypto Market Cap Explained for the broader framework.

Why beginners misjudge stablecoin risk

One of the more common beginner mistakes is treating all stablecoins as equivalent. They share a name and a nominal $1 price target, but the risk profiles are substantially different.

A stablecoin issued by a regulated company, backed by audited cash and short-term U.S. government securities, with clear redemption terms and regulatory oversight, carries meaningfully lower peg risk than a stablecoin maintained by an algorithmic mechanism with no direct backing. Treating them as interchangeable because both currently trade at $1.00 misses the entire question of what happens when they are under stress.

The relevant questions are not about the current price. They are about the mechanism: What holds the peg? How transparent is the backing? What is the redemption process, and how long does it take? What happens to the mechanism when the market moves sharply against it? Has the issuer been audited, and by whom? What regulatory framework covers the issuer?

Another common error is assuming that because a stablecoin has held its peg through normal conditions, it will hold through extreme ones. Stability during calm markets is not the same as stability under stress. Some mechanisms that appear functional for years are revealed to be fragile only when conditions shift rapidly. The design matters more than the track record.

Readers who want to evaluate crypto assets and protocols more rigorously should see How to Research a Crypto Coin Properly and What Is Tokenomics?, which covers how economic design choices — including the ones that govern stablecoin mechanisms — affect long-term stability.

How to think about stablecoin risk more carefully

For most readers, the practical goal is not to become an expert in stablecoin mechanism design. It is to avoid holding a significant portion of value in a stablecoin that is more fragile than it appears.

The starting point is understanding the category. Fiat-backed stablecoins from regulated issuers with high-quality reserves and clear redemption terms are the lowest-risk category in normal conditions. Crypto-backed stablecoins with substantial over-collateralization and transparent, battle-tested liquidation mechanisms occupy a middle tier. Algorithmic stablecoins, particularly newer ones without a long stress-test history, carry substantially higher peg risk and are generally not appropriate for storing value at scale.

Reserve quality matters within the fiat-backed category as well. Not all fiat-backed stablecoins hold equivalent reserves. The composition of the reserve — whether it is held in cash, short-duration government securities, commercial paper, or less liquid instruments — affects how quickly and reliably it can be liquidated to meet redemptions under stress. Attestation reports and audit transparency are the primary tools for evaluating this from the outside.

Redemption mechanics are underappreciated as a risk factor. Even if a stablecoin is well-backed, the ability to redeem at face value depends on the issuer’s process, minimums, timelines, and operational capacity. A small retail holder often cannot redeem directly with the issuer at all — they are dependent on secondary market pricing, which can deviate during stress.

Concentration risk is the final layer. Holding any single stablecoin exclusively creates a single point of failure if that issuer or mechanism is impaired. Many experienced market participants maintain exposure across multiple stablecoin types for this reason.

For readers earlier in their crypto learning path, this topic fits naturally after Crypto for Beginners and before moving into more complex DeFi or investing decisions.

Practical warning signs to watch

Stablecoin risk usually becomes obvious after the price has already moved. The better habit is to watch the conditions around the peg before the market forces a decision.

The discount is persistent, not momentary. A brief move to $0.998 during heavy trading is normal. A discount that widens, lasts through multiple trading sessions, or fails to close when arbitrage should be profitable deserves closer attention.

Redemptions are delayed or unclear. If holders cannot redeem directly, if minimum redemption sizes exclude most users, or if the issuer gives vague updates during stress, the secondary market will price that uncertainty. A stablecoin can be fully backed in theory and still trade below peg if holders cannot access redemption reliably when it matters.

Exchange liquidity thins out. The order book matters. A stablecoin may still show a near-$1 price on a calm exchange while large holders are unable to exit without moving the market. Widening spreads, vanishing bids, or sharp differences between venues suggest the peg is being defended by thin liquidity rather than broad confidence.

Reserve quality becomes the question. High-quality, short-duration, liquid reserves are easier to convert into cash quickly. Long-duration, opaque, illiquid, or credit-sensitive assets are harder to sell under pressure. Once the market starts debating the reserve, the stablecoin has already moved from routine operation into confidence management.

The problem spreads into DeFi or exchange settlement. A small discount can become systemic if lending protocols, liquidity pools, or exchanges continue treating the stablecoin as exactly $1.00 while the market does not. That mismatch creates liquidations, bad debt, and incentives for faster exits.

Regulation is part of this risk framework because stablecoin rules usually focus on the same issues: issuer quality, reserve composition, redemption rights, disclosure, and supervision. Crypto Regulation: How It Works explains why stablecoins often sit on their own regulatory track rather than being treated like ordinary speculative tokens.

Frequently asked questions

What does it mean when a stablecoin loses its peg? It means the token is no longer trading at the value it is supposed to track — most often $1.00. Small deviations of a fraction of a cent are normal market microstructure. A real depeg is when the price moves meaningfully below the anchor and the mechanism designed to restore the peg is under visible stress.

Is every move below $1.00 a depeg? No. A stablecoin trading at $0.998 or $1.002 during normal conditions is inside the routine band most fiat-backed stablecoins move within. The signal worth paying attention to is whether the deviation is widening, persistent, and accompanied by selling pressure that the peg mechanism is not absorbing.

Why do some depegs recover and others spiral? Recovery depends on confidence in the mechanism. A well-reserved stablecoin where redemption is functioning can usually trade back to $1.00 once redemption pressure eases. A stablecoin where the market has stopped believing the design will hold tends to spiral, because participants sell into the discount instead of buying it.

Are algorithmic stablecoins more likely to depeg than fiat-backed ones? Historically, yes. Algorithmic designs depend on participants believing the incentive mechanism will defend the peg. When that belief fails, the mechanism that was supposed to restore $1.00 can accelerate the collapse. Fiat-backed stablecoins from regulated issuers with audited reserves carry meaningfully lower peg risk in normal conditions, though they are not risk-free.

Can a depeg affect coins I hold even if I do not own the stablecoin? Yes. Stablecoins are used as collateral in DeFi protocols, as the settlement layer on exchanges, and as the dominant trading pair for most altcoins. A serious depeg can trigger forced liquidations, exchange disruption, and broader risk-off selling that pressures the entire crypto market.

How can I reduce stablecoin risk? Understand what holds the peg before holding the token. Prefer fiat-backed stablecoins from regulated issuers with transparent reserve disclosures, redemption rights, and a track record through stress. Avoid concentrating large balances in a single stablecoin. And recognise that the word “stable” describes an intent, not a guarantee.

The label is not the guarantee

The word “stablecoin” describes an intent, not an outcome. Every stablecoin is a bet that its mechanism will hold under the full range of conditions the market can generate — not just the mild ones. Some of those bets have strong foundations: well-reserved, transparently audited, backed by regulatory frameworks, and designed with redemption pressure in mind. Others do not.

A depeg is what happens when the bet fails. The severity ranges from a brief, self-correcting discount to a complete and irreversible collapse of the design. The difference lies in whether the underlying mechanism is sound and whether confidence in that mechanism can be restored once it is under pressure.

Treating stablecoins as cash equivalents, without understanding what holds the peg, is one of the more common ways that otherwise cautious crypto participants take on more risk than they intended to. The name is the same. The risk is not.