Almost every week, a crypto headline turns on a regulatory question. A bill advances. An agency files a case. An ETF is approved or delayed. A stablecoin issuer is told to register, restructure, or wind down. A foreign jurisdiction publishes a new framework, or rolls one back.

For readers, the difficult part is not finding regulation news. It is making sense of it. Different headlines describe different regulators, different countries, different stages of a rulemaking process, and different parts of the crypto market. They are often presented as if they were the same kind of event, when in practice they are not.

This guide builds a practical mental model for how crypto regulation actually works. It is written for readers who follow Bitcoin, Ethereum, stablecoins, ETFs, exchanges, and market-structure stories, and who want to understand the framework well enough to interpret news rather than react to it. It is not legal advice and does not take a position on any particular bill, agency action, or political debate.

What “crypto regulation” actually covers

When people say crypto regulation, they usually mean a single thing — a vague rulebook that governs the industry. In practice, regulation is the sum of many separate pieces of authority, each one covering a specific kind of activity.

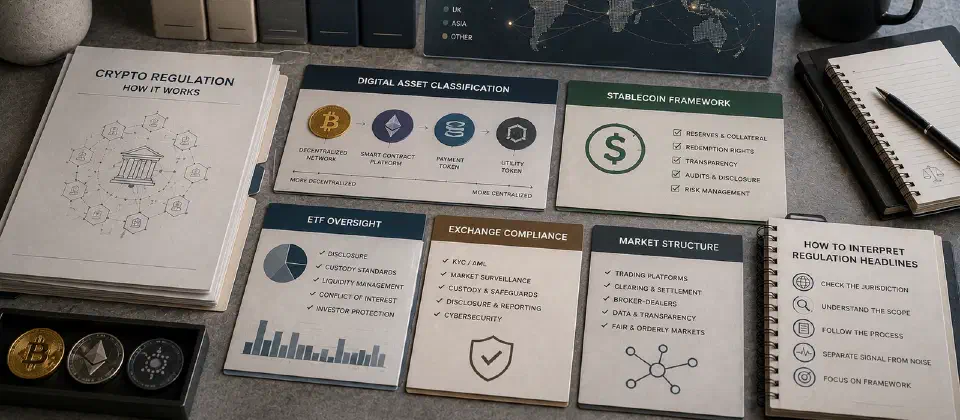

In broad terms, crypto regulation involves rules about:

- Tokens and their classification. Is the asset a security, a commodity, a payment instrument, a collectible, or something new? Different categories trigger different rules.

- Exchanges and brokers. Registration, market-integrity standards, custody requirements, anti-money-laundering controls, customer-asset segregation, and reporting obligations.

- Stablecoins. Reserve composition, redemption rights, issuer transparency, audit standards, and treatment of stablecoins inside the payments system.

- Custody. How regulated firms hold customer crypto, what fails if they go insolvent, and how those assets must be ringfenced.

- Disclosure. What issuers, exchanges, ETFs, and public companies must tell investors about their crypto exposure, risks, and controls.

- Anti-money-laundering and sanctions. Identity-verification requirements, suspicious-activity reporting, and obligations on intermediaries.

- Taxation and reporting. How crypto is taxed, who must report transactions, and how brokers must furnish information.

- Market abuse and consumer protection. Rules against manipulation, fraud, misleading marketing, and unsuitable products.

A regulation headline is almost always pointing at one of these slices, not at all of them. Reading regulation news well begins with asking which slice before asking how big a deal is this.

Why crypto is hard to fit into existing rules

Most financial regulation was designed for a world where assets came in well-defined categories. There were stocks, bonds, commodities, currencies, and a small set of derivatives. Each category had a regulator, a market structure, and a set of disclosure obligations. New products generally fit somewhere on the existing map.

Crypto resists that map. A single token can carry traits from several categories at once. Bitcoin behaves like a commodity in some respects, like a payments network in others, and like a speculative asset in still others. Many later tokens combine features of software, governance rights, network access, payment, and investment exposure. Stablecoins look like deposits, money-market instruments, and payment tools simultaneously. NFTs can resemble collectibles, licensing rights, or — in some structures — investment products.

Several other features make the category harder to handle:

- Decentralization. A network without a central issuer or operator does not have an obvious party to register, license, or fine.

- Self-custody. Assets can move directly between individuals without an intermediary that regulators can supervise.

- Cross-border activity. A protocol can be developed in one country, used in another, and offer access from almost everywhere.

- Fast product innovation. New token structures, new market venues, and new product wrappers appear faster than rulemaking processes typically run.

None of this makes crypto unregulated. It means that fitting crypto into existing rules is genuinely hard, and that regulators in different jurisdictions reach different conclusions about how to do it. That is why one headline can describe crypto as tightly regulated and another can describe the same market as a regulatory gray zone — both can be partly true at the same time.

The questions every regulation story is really about

Behind almost every regulation headline is one or more of a small set of recurring questions. Holding these in mind makes news much easier to parse.

- Classification. Is this asset, in this jurisdiction, considered a security, a commodity, a payment instrument, or something else?

- Authority. Which regulator is in charge of supervising this activity, and is that authority clear or contested?

- Disclosure. What must issuers, exchanges, or product sponsors tell investors and the public, and how often?

- Market structure. Who can run an exchange, broker, or market maker, and what standards must they meet?

- Stablecoin oversight. Who issues, who supervises, what reserves are required, and what redemption rights customers have.

- Custody and segregation. How are customer assets held, who is responsible if a firm fails, and what protection exists.

- DeFi and self-custody. Where do non-custodial protocols and individual wallet users sit in the framework?

- Cross-border reach. Does the rule apply only to domestic users, to firms targeting domestic users, or more broadly?

A useful first question on any regulation story is: which of these is this story actually about? Many headlines blur the answer because the underlying details are technical and the political surface is more interesting.

The most practical interpretation framework is to separate the asset, the activity, and the venue. The same token can be treated differently depending on whether it is being sold by an issuer, traded on a platform, used in a DeFi protocol, held by a custodian, wrapped inside an ETF, or used as payment collateral. Regulation rarely answers “is this crypto legal?” in one sentence. It usually answers a narrower question: who is doing what, for whom, through which structure, and under which jurisdiction.

SEC, CFTC, and U.S. market structure

In the United States, two agencies sit at the center of most crypto market-structure debates: the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC). Other regulators — banking agencies, the Treasury, state regulators, and the IRS — also matter, but they tend to come into the story for narrower questions.

In broad terms:

- The SEC supervises securities markets — stocks, bonds, investment funds, and securities offerings. Its core toolkit is registration, disclosure, and anti-fraud enforcement. When the SEC engages a crypto issue, the underlying question is usually whether a token, product, or platform involves a security under U.S. law.

- The CFTC supervises commodity derivatives markets — futures, options, and certain swaps. It also has anti-fraud and anti-manipulation authority over commodity spot markets. When the CFTC engages a crypto issue, the question is usually whether the asset is a commodity and whether the activity involves regulated derivatives or manipulative behavior.

The reason U.S. market-structure legislation matters is that the existing split between these agencies was not designed for crypto, and the resulting boundary disputes have produced a long-running debate about which agency should oversee which part of the market. Periodic legislative efforts try to redraw that boundary and to define which crypto assets fall under each agency’s authority. The names of the bills change, the political balance shifts, and the proposals are revised, but the underlying question is consistent: who supervises what.

When you read a story about a U.S. crypto market-structure bill, the practical questions to ask are:

- Has the bill been introduced, marked up, voted out of committee, passed in one chamber, or signed into law?

- Does it primarily address classification, exchange registration, stablecoin oversight, or all of the above?

- What is the implementation timeline if it does pass?

- Does it preempt state rules or layer on top of them?

Many readers conflate proposed with passed, and passed with in force. Each step is a long way from the next. A bill in markup is not a regulatory regime, even if the headlines treat it as one.

Stablecoin regulation

Stablecoins are usually regulated as their own category, and for good reason. A token that promises to maintain a fixed value — whether one dollar, one euro, or another reference — sits closer to deposits, money-market funds, and payment instruments than to a speculative crypto asset. That places it in regulatory territory that traditional financial supervisors have always cared about.

Stablecoin rulemaking, in any jurisdiction, generally focuses on a few questions:

- Who can issue. Banks, regulated trust companies, licensed payment institutions, and similar entities are the usual candidates. Some frameworks allow non-bank issuers under specific conditions; others restrict issuance to a narrow set of regulated firms.

- What can back the stablecoin. Reserves are typically expected to be high-quality, liquid, and conservatively managed — short-term government instruments, central-bank deposits, and similar. Riskier or illiquid backing is usually disallowed or limited.

- How redemption works. Holders are generally expected to be able to redeem stablecoins at face value within defined timeframes, with the issuer required to honor requests under stated conditions.

- What disclosures are required. Reserve composition, audit results, and material risks are usually expected to be published on a regular cadence.

- How the issuer is supervised. Examination, capital, governance, and operational standards similar to those that apply to other regulated payment or banking firms.

The deeper reason for separate stablecoin regulation is systemic. Large stablecoins effectively become privately issued payment instruments that millions of people treat as money. That places them at the intersection of banking, securities, and payments policy, which is why the rules tend to be both detailed and politically contested. For a fuller introduction to how stablecoins are constructed and used, our guide on what stablecoins are provides the foundation, and the stablecoin depeg guide explains why even well-designed stablecoins can fail under stress.

ETFs and regulated market access

Spot crypto ETFs are one of the most visible regulatory stories of the cycle. Their importance is usually framed in price terms, but the more durable change is structural: an ETF wrapper places a crypto asset inside the same regulatory plumbing as any other listed fund. That has effects in several directions at once.

For investors, an ETF means crypto exposure can be held in regulated brokerage accounts, retirement accounts, and managed portfolios that could not previously hold native crypto. Regulated custody, audit, and disclosure requirements come along by default. The product is bought and sold through familiar market infrastructure rather than through a crypto-native exchange.

For regulators, an ETF means a transparent, supervised wrapper sits between the underlying market and the typical investor. Surveillance-sharing arrangements with major venues, custody standards for the underlying asset, and disclosure obligations from the issuer all come into play.

It is important to be precise about what ETF approval does and does not mean. Approval of a spot ETF for a particular asset does not mean every crypto asset is approved. It does not extend the same regulatory comfort to other tokens. It does not turn lightly regulated venues into fully regulated ones. It says, for one specific asset and one specific product structure, the regulator concluded that an ETF could be offered to the public with a defined set of disclosures, custody arrangements, and market-surveillance terms.

For a deeper view of what ETFs structurally changed about Bitcoin’s market, our guide on how Bitcoin ETFs change price, liquidity, and market structure walks through the mechanics in detail. The companion guide on how to read crypto ETF fund flows explains how to interpret the daily flow data without overreacting to single readings.

Exchanges, custody, and investor protection

Exchanges and custody firms are where most retail and institutional crypto activity actually happens, which is why they sit close to the center of regulation in nearly every jurisdiction.

Typical exchange-level expectations include:

- Registration or licensing. Operating an exchange, brokerage, or money-services business usually requires a license appropriate to the activity in the relevant jurisdiction.

- Anti-money-laundering and sanctions controls. Customer identity verification, transaction monitoring, suspicious-activity reporting, and screening against sanctions lists.

- Custody and segregation. Customer assets are typically expected to be held separately from the firm’s own funds, with controls and disclosures about how those assets are stored.

- Market-integrity standards. Surveillance for manipulation and abuse, fair-access rules, and limits on conflicts of interest.

- Disclosure to customers. Information on fees, conflicts, custody arrangements, and material risks.

The practical case for these rules became more concrete after several major exchange failures in earlier cycles. When customer assets were not properly segregated, when conflicts of interest between trading and lending desks were not disclosed, or when custody and risk controls were weak, customers absorbed the losses. Regulation in this area is largely a response to that history.

Educational coverage of exchange regulation should keep two things in mind. First, regulated does not equal safe — a regulated firm can still take losses, suspend services, or go through restructuring. Second, unregulated does not equal dangerous in every case — but it does mean fewer protections by default. The honest framing is that regulation reduces certain failure modes without eliminating market risk.

For readers evaluating a platform, the practical questions are straightforward: are customer assets segregated, who controls private keys, what disclosures explain conflicts of interest, what happens if the company fails, and which regulator can enforce the rules? Those questions matter more than the marketing label a venue uses for itself.

Global regulation and why it differs

Crypto regulation is not a single global standard, and it is unlikely to become one. Different regions have different priorities, different legal traditions, and different relationships between their financial regulators.

In broad strokes:

- Europe has moved toward a comprehensive, harmonized framework across member states that defines categories of crypto-asset activity and licenses providers operating across the region. Stablecoins, exchanges, custody, and disclosure obligations sit inside that framework.

- The United Kingdom has its own evolving framework that focuses on bringing crypto activity into existing financial-services rules with specific adjustments for digital assets.

- East Asia is highly varied. Some jurisdictions have built detailed exchange-licensing regimes, stablecoin frameworks, or institutional access rules; others have taken a much more restrictive posture toward retail trading or token issuance.

- The Middle East includes several jurisdictions that have established dedicated crypto-asset regulators and active licensing regimes, alongside others that take a more cautious view.

- Other regions range from active permissive frameworks to outright restrictions, with many countries still publishing or revising their first comprehensive rules.

The reason these differences matter for ordinary readers is that they affect access, liquidity, and product availability. The same exchange may serve users in some countries and not others. The same stablecoin may be available in some markets and restricted in others. The same ETF may be sold in some jurisdictions and not approved in others. A global crypto market is built on top of a fractured regulatory map, and that fracture shows up in the products available to a given user.

How regulation actually affects crypto markets

Regulation affects crypto markets through several channels, and each one runs on a different timeline.

- Access. Clearer rules can let new categories of investors and institutions participate — pension funds, insurance portfolios, wealth managers, retirement accounts. That broadens the demand base, often slowly.

- Liquidity. When regulated venues, custodians, and products grow, market depth typically improves at the regulated layer. Spreads tighten, larger orders become easier to execute, and intraday volatility can ease in normal conditions.

- Product availability. Some products, services, or venues get added when rules clarify; others get removed or restricted. The net effect is a constantly reshaping menu of what users in a given jurisdiction can actually do.

- Sentiment. Regulation affects perception faster than it affects substance. A favorable headline can lift sentiment in advance of any rule actually being implemented; an enforcement action can pressure sentiment even when its long-term legal outcome is unclear.

- Tail-risk reduction. Stricter custody, disclosure, and market-integrity rules can lower the probability of certain catastrophic failures — segregation failures, hidden conflicts, undisclosed insolvencies — without removing market risk.

What regulation does not do is set a price floor or guarantee adoption. A market with strong rules can still see drawdowns, capital outflows, and product failures. The honest framing is that regulation shapes the structural environment in which prices move, not the direction of prices themselves.

Common mistakes when reading regulation news

A handful of recurring mistakes account for most overreactions to regulation headlines:

- Confusing proposed with passed. A bill introduced or under markup is not a law. Most regulatory proposals are revised heavily before becoming law, and many never do.

- Confusing passed with in force. Even after a law is signed, implementation often takes months or years through regulator rulemaking and transition periods.

- Treating ETF approval as universal. Approval for a specific asset and structure does not extend to other tokens or other product types.

- Generalizing across jurisdictions. A rule in one country, region, or state does not automatically apply elsewhere, and may not be representative of the global picture.

- Treating enforcement as final law. A complaint, charge, or initial decision is one stage in a long process — not a settled legal conclusion.

- Assuming regulation guarantees price gains. Clearer rules can support participation, but they do not remove drawdowns or guarantee returns.

- Conflating stablecoin rules with broader crypto rules. Stablecoin frameworks usually move on their own track and do not necessarily speak to how tokens, exchanges, or DeFi will be treated.

- Ignoring scope. A rule that targets one product, one issuer, or one venue is not a market-wide regime change, even if the headline implies otherwise.

Most of these mistakes share a common shape: the headline compresses several layers of nuance into a single dramatic claim, and the reader processes it as if all those layers were settled. Slowing down to ask which stage, which jurisdiction, and which slice of the market is involved fixes most of them.

A simple regulation-news reading checklist

When a regulation story appears, a short pass through these questions will usually surface its real weight.

- What stage is this? Discussion, proposal, markup, vote, signed law, rulemaking, implementation, enforcement, appeal? Each implies a different distance from real-world impact.

- Which regulator or jurisdiction? Federal or state? Securities, commodities, banking, payments, or tax? Domestic or extraterritorial?

- Which slice of the market does it touch? Tokens, exchanges, brokers, stablecoins, ETFs, custody, DeFi, public-company disclosure, or taxation?

- Is the rule final or open for input? Many rules go through public consultation and are revised before they become binding.

- Does it change access, reporting, custody, liquidity, or issuer obligations? Different categories affect the market in different ways.

- Is the market reacting to fact, expectation, or uncertainty? Sometimes the move is about the rule itself; sometimes it is about how the rule changes assumptions.

- Is the impact narrow or broad? A rule on one product, one issuer, or one venue is not the same as a market-wide regime change.

- What does the regulation imply for connected parts of the market? A stablecoin rule can affect on-ramps, exchanges, and ETF custody indirectly. A custody rule can affect which products are viable.

Used together, these questions produce a much steadier reading than a snap reaction to the headline.

What regulation does not tell you

Regulation is one of several major forces shaping crypto markets. It is not the only one.

Macro conditions — interest rates, dollar strength, liquidity in the broader financial system — push and pull on risk assets in ways that often dominate regulation news in the short term. Our guide on how interest rates affect Bitcoin and crypto walks through those channels in detail.

Bitcoin’s own cycle dynamics, network fundamentals, and on-chain activity also matter. A favorable regulatory backdrop in a tightening macro environment can still see meaningful drawdowns; a difficult regulatory backdrop in an easing macro environment can still see strong rallies. Internal market dynamics — captured in indicators like Bitcoin dominance and the broader four-year cycle — interact with regulation rather than being overridden by it.

For readers building a foundation, the crypto for beginners guide is a sensible starting point, and how to thoroughly research a crypto coin extends the disciplined reading habit beyond regulation news.

The honest summary is that regulation matters, but it sits inside a wider system. The point of understanding the framework is not to predict the next price move from the next headline. It is to understand which headlines are real changes, which are early signals, and which are noise — and to make better-informed reading decisions across the full crypto market.

Frequently asked questions

Is crypto legal? In most major jurisdictions, holding, buying, and selling crypto is legal, often inside a defined framework. Specific activities — running an unlicensed exchange, issuing certain tokens to retail investors, offering particular products without registration — can be restricted or prohibited. The honest answer is that crypto itself is generally legal, but the activities around it are regulated, and the rules differ by country and by activity.

Who regulates crypto in the United States? There is no single regulator. The SEC handles securities-law questions, the CFTC handles commodity-derivatives and certain spot-market integrity questions, banking agencies handle bank involvement and stablecoin-adjacent activity, the Treasury and FinCEN handle anti-money-laundering, the IRS handles taxation, and state regulators handle money-transmission and additional consumer-protection rules. Most legislative debates about U.S. crypto market structure are about clarifying how these jurisdictions divide.

Are Bitcoin and Ethereum regulated the same way? Not always. Bitcoin is widely treated as a commodity in U.S. derivatives markets, and a spot Bitcoin ETF has been approved at the federal level. Ethereum’s classification has been debated more openly, and its product approvals and treatment have followed a different path. Outside the U.S., the answer depends on the local framework. Treating both assets as identical in regulatory terms is a common but inaccurate shortcut.

Does ETF approval mean crypto is fully regulated? No. An ETF approval applies to a specific asset and a specific product structure. It does not extend the same regulatory comfort to other tokens, to derivatives, to DeFi, or to native crypto exchanges. ETF approval is a meaningful structural development, but it is narrower than headlines often suggest.

Why do stablecoins have separate rules? Because they behave more like deposits, money-market instruments, and payment tools than like speculative crypto assets. Holders expect them to keep a fixed value, which raises questions about reserves, redemption rights, issuer transparency, and broader payment-system stability that regulators have traditionally cared about. That makes stablecoins their own regulatory category, often supervised under banking or payments rules rather than securities rules.

Can regulation make crypto safer? It can reduce certain failure modes — undisclosed conflicts of interest, custody mismanagement, fraudulent offerings, market manipulation — by raising standards and providing recourse. It does not eliminate market risk, technology risk, or liquidity risk, and it cannot guarantee that any specific asset or product will succeed.

Does regulation always help prices? No. Clearer rules can support participation and reduce structural friction over time, but the immediate price reaction to a regulatory event depends on expectations, scope, and macro context. Some favorable rules pass with little price reaction because they were already expected; some stricter actions pressure prices only briefly. Treating regulation as a one-way directional signal is one of the most common mistakes in this category.